Power emerges as new battleground for Indonesia's nickel smelters

Tuesday, June 9 2026 - 08:51 AM WIB

By Dominikus

Indonesia's nickel pig iron (NPI) industry may be entering a new phase in which access to electricity becomes as important as access to ore, as aluminum projects offer significantly higher returns per unit of power than NPI production in integrated industrial parks, according to Thomas Feng, Head of Nickel-Cobalt-Lithium Industry Research at Shanghai Metals Market (SMM).

Speaking at the Indonesia Critical Minerals Conference in Jakarta last week, Feng said aluminum could generate about 36 times more gross profit per MWh than NPI under SMM's assumptions. The disparity raises the prospect that industrial park operators facing power constraints may prioritize aluminum production over NPI smelters.

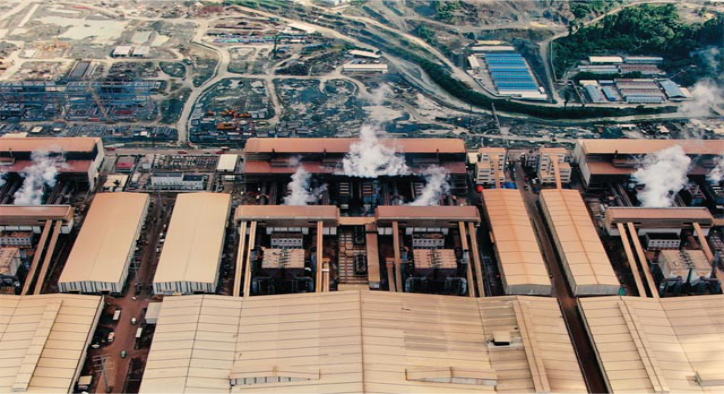

The issue is particularly relevant as Indonesia's industrial parks host a growing mix of pyrometallurgical nickel operations, high-pressure acid leach (HPAL) facilities, aluminum smelters and supporting industries competing for the same electricity supply.

SMM's analysis of Indonesia Weda Bay Industrial Park identified a transition-period power gap of around 300-700 GWh per month. Feng described the situation as a "smelter first, genset later" mismatch, where industrial capacity expands faster than power infrastructure.

For investors, stainless steel producers and industrial park operators, the implication is that NPI competitiveness can no longer be evaluated solely on ore reserves, production capacity or nickel prices. Power availability, captive generation schedules and electricity allocation are becoming increasingly important determinants of supply reliability and profitability.

SMM said NPI margins are already close to cash-cost levels, meaning even modest declines in nickel prices could push some operations into negative returns on power consumption. Under such conditions, aluminum projects may gain priority because they generate substantially higher economic value from each unit of electricity.

The potential impact on nickel supply could be significant. Feng estimated that diverting just 15% of available capacity could reduce NPI output by around 5%. A 5%-15% decline in production could tighten supplies to China, support NPI prices and increase procurement pressure on Chinese stainless steel mills.

The importance of NPI extends beyond Indonesia. Veronique Steukers, President of the Nickel Institute, said NPI has become the dominant nickel feedstock for global stainless steel production, accounting for more than 80% of the sector's primary nickel requirements. Together, NPI and ferronickel represent more than 90% of primary nickel consumption in stainless steel.

Nickel Institute data show stainless steel remained the largest end-use sector for nickel in 2024, accounting for 66% of first-use demand, compared with 16% for batteries, 6% for nickel alloys, 5% for plating, 3% for alloy steels, and smaller shares for foundries and other applications.

At the same time, Indonesia's NPI industry is facing declining ore quality. SMM projects average furnace-feed nickel grades will fall from 1.75% in 2023 to 1.45% by 2030, while average NPI nickel content could decline from 12.9% to 10.7%.

The share of NPI containing more than 14% nickel is expected to fall from 17% to 2%, while lower-grade 8%-10% NPI could rise from 8% to 28% of total output.

According to Feng, declining saprolite grades could increase ore consumption by around 30%, raising production costs and reshaping grade premiums. Combined with growing competition for power from aluminum projects, the NPI industry faces a more challenging margin environment than suggested by ore supply concerns alone.

SMM expects tightness in high-grade NPI supply to peak in 2027 before easing after 2028 as stainless steel scrap, refined nickel and ferronickel substitution become more widely available. Until then, ore quotas, declining grades and power constraints are expected to keep the market tight and support prices.

The broader takeaway is that Indonesia's nickel downstreaming story is becoming increasingly tied to industrial infrastructure. As nickel, aluminum, HPAL facilities and power generation projects expand within the same industrial zones, future growth may depend as much on electricity availability as on mineral resources.

Editing by Reiner Simanjuntak